The straightforward bookkeeping platform for sole traders.

The all-in-one accounting software that’s easy to use, built for small businesses.

No accounting experience needed.

Free 30 day trial. No credit card required.

Exciting News:

okke joins the Reckon Accounting Software family

Save time, reduce hassle, and focus on growing your business

okke offers all the features you need without limits on invoices, customers, or your earnings. Spend less time and money on bookkeeping, and focus on what you do best – growing your business.

I still remember those dreadful hair-pulling, caffeine-inducing half-a-day quarterly spreadsheet rituals. Now, it’s just me, okke and a breezy 20 minutes.

Chau L.

Pixel HeroFriendly price - that makes sense.

Sign up today.

okke

$19/month

All-in-one accounting for sole traders and solo business owners.

Unlimited support. Cancel anytime.

$209/year

All-in-one accounting for sole traders and solo business owners.

Unlimited support. Cancel anytime.

Key features:

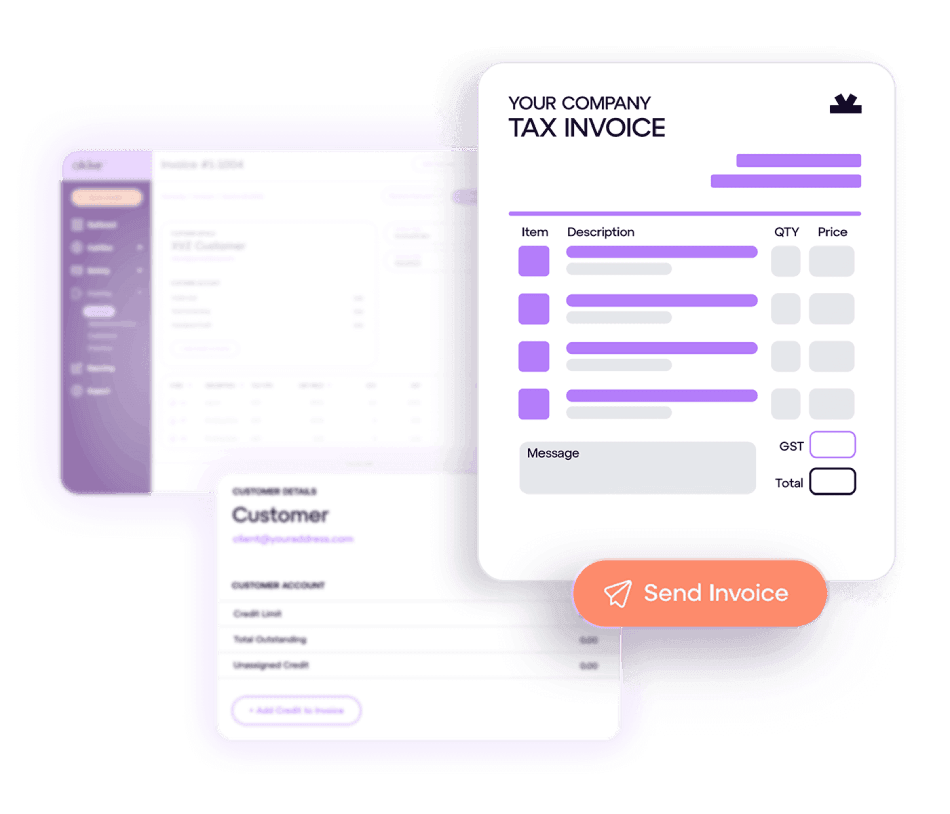

- Send invoices and quotes Unlimited

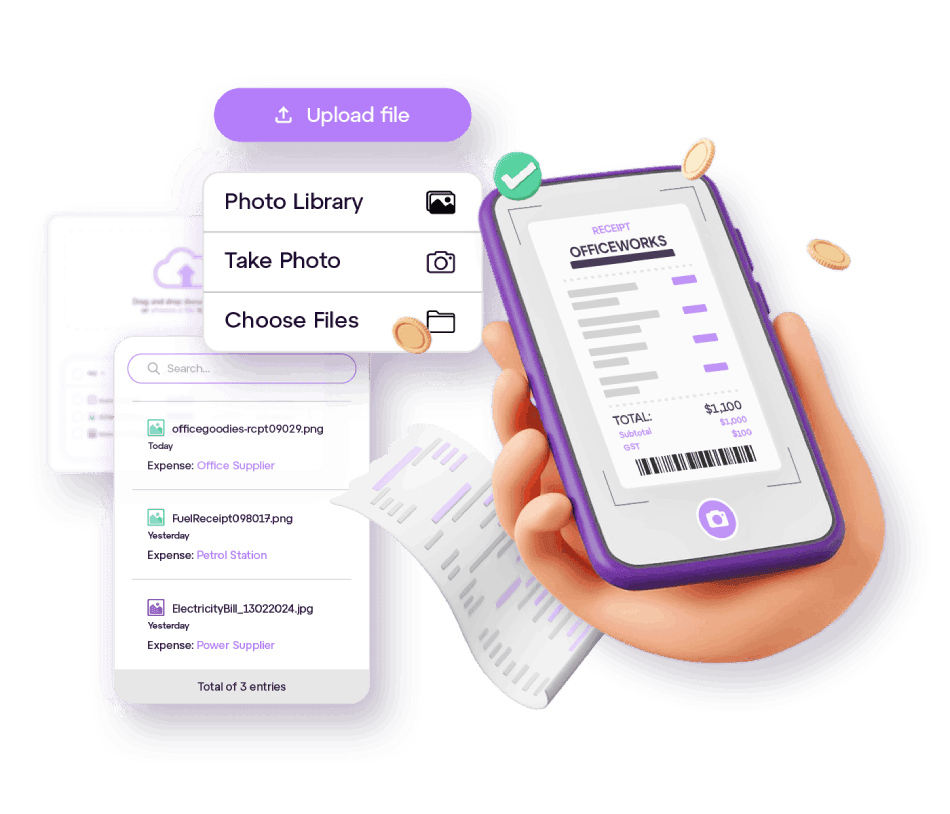

- Track income and expenses Unlimited

- Manage your customers Unlimited

- Automatic payment reminders

- Connect your bank accounts

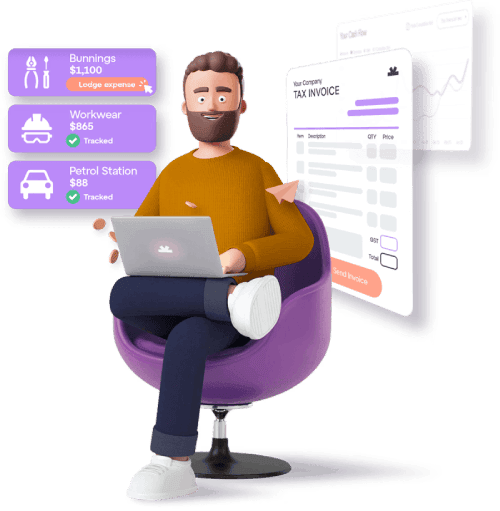

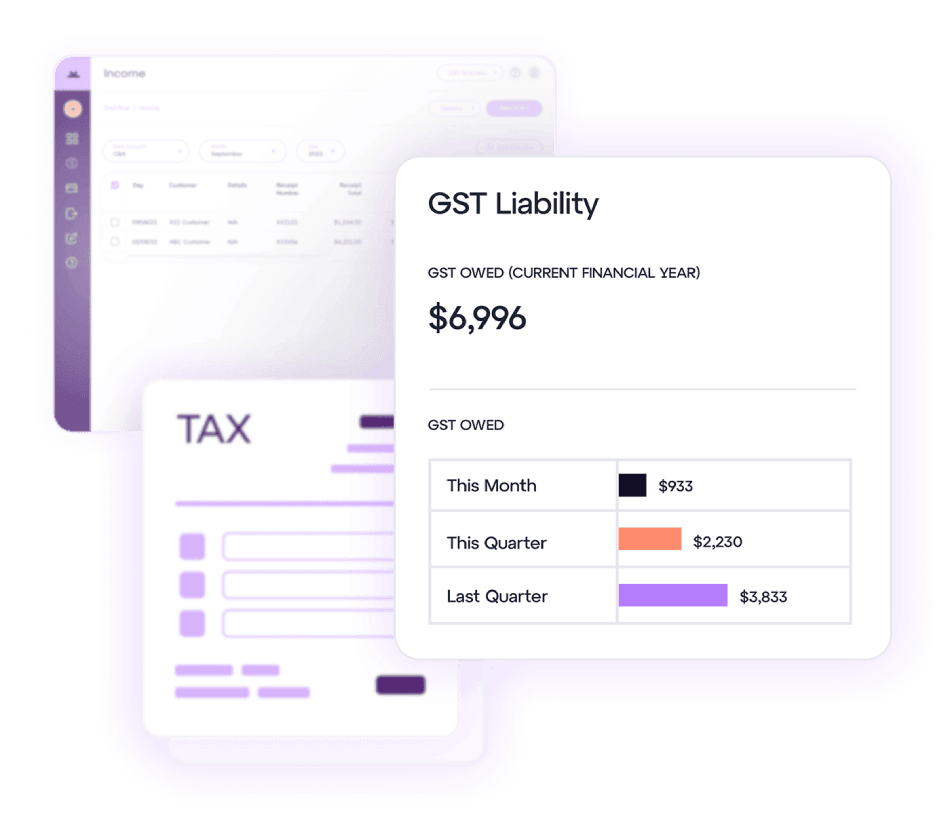

- Tax and GST tracking

- Business reports and insights

- Keep digital copies of your receipts

Key features:

- Send invoices and quotes Unlimited

- Track income and expenses Unlimited

- Manage your customers Unlimited

- Automatic payment reminders

- Connect your bank accounts

- Tax and GST tracking

- Business reports and insights

- Keep digital copies of your receipts

Why sole traders choose okke for their bookkeeping

More time

for your business

More time

for your business

You can replace the late nights, weekend admin and stress headaches with automatic bank transactions, fast invoicing and instant reports.

Automate invoicing

Automate invoicing

okke gets you paid faster thanks to online payments and automatic tracking. Send invoices instantly and without drama.

Have full confidence to launch your business

Have full confidence to launch your business

Join 4000+ Aussies that have trusted okke

The generous trial period was extremely helpful when starting out. The setup is so smooth and everything works right out of the box. Within minutes of signing up, I was able to send a fully compliant invoice to my first NDIS support client.

I love okke as it is so easy and simple to use... it makes invoicing a dream. It is also incredibly useful for tracking any relevant expenses that are used for my business.

okke is so easy, it allows me to spend more time on my creative work and less time doing the boring (but always important) admin and billing.

So simple to use, especially for a non-accounting person like me - I love it. Have even showed my teens how to use it to keep track of their little businesses.

It’s very user friendly and easy to navigate, and convenient for a small business starting out who don’t have the funds to invest in expensive invoicing software.

Frequently asked questions

Frequently asked questions

Want to stay in the loop?

Sign up to get our non-annoying email updates.